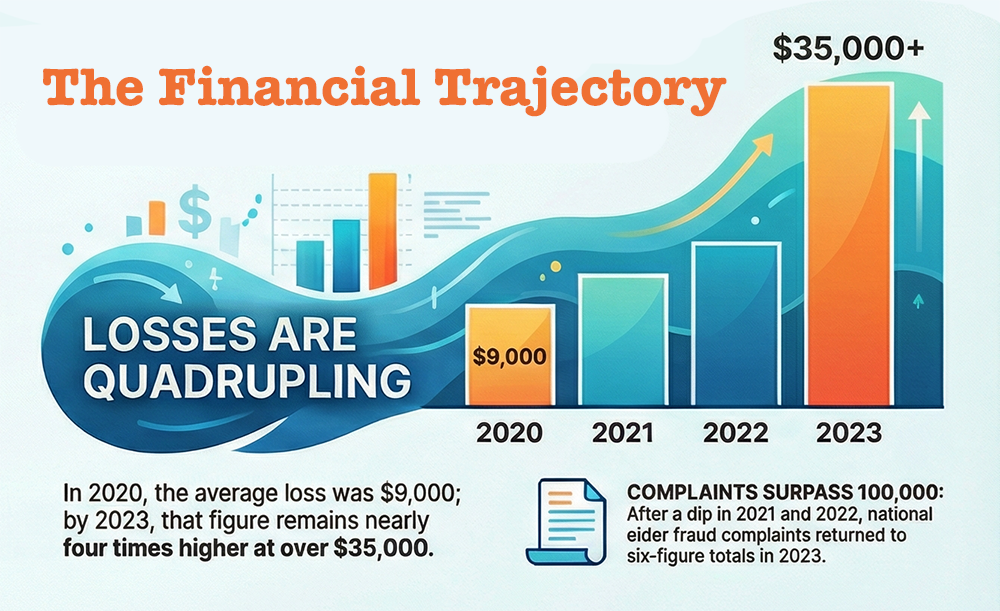

Not to scare the tar out of you, but in the past two years, 75% of adults age 50-80 reported experiencing a scam attempt and 30% experienced fraud.

Now that your gulp is over, it's time to face it: fraud is a way of life for some and for us on the other end, it's is an unfortunate reality. Just look at how fast it's growing...

However, losing money is not inevitable. It's preventable.

The most effective fraud prevention for seniors comes from good 'ol preparation, clear communication, and everyday sensible habits that support financial safety—without us losing our wits.

Take it from a senior who lost her entire ... life ... savings:

Prevention: More Important Than Recovery? Yes.

Once a scammer has fleeced you of your savings or money of any kind, you can pretty much kiss it goodbye because recovering it can be difficult—if not completely impossible.

Truth hurts: Banks are basically powerless; so are the police. And that's why fraud prevention is most effective when seniors take steps early, before a problem occurs.

And it doesn't take going back to school to learn how to prevent fraud, either.

Take two minutes to read our Anatomy of a Scam. It could save you a lot of stress when the time comes.

Pre-Emptive Protections That Make a Difference

Many protections are simple and do not interfere with daily life. Small actions can add strong layers of security.

Helpful fraud prevention for seniors includes:

Keeping your personal information to yourself: Your account numbers are no one else's business for the most part so, if someone asks you for details like account numbers or identification, make sure you a) know them; b) trust them and that you give them this info only when absolutely necessary.

Using simple account alerts: Alerts for unusual activity can provide early awareness. Set up the notifications on your phone for every transaction from a penny up. Scammers start low with their rip-offs (like under $10) and that's how they start to bleed your accounts. It may seem like a nuisance, but stopping a scam early when it's $7 is a lot better than when it's $70.

Limiting the number of financial accounts: Fewer accounts are easier to monitor and manage. Ask yourself – "How many credit cards do I really need?".

Keeping documents organized and secure: Important papers should be stored safely and reviewed occasionally. Odd as it may seem, some smartpants seniors put their most valuable paperwork in the ... freezer. Why? Because they a) know where it is; b) it's safe if there's ever a fire.

Taking time before making financial decisions: Pressure is often a warning sign. If someone (meaning a potential scammer) asks you for some account info, put 'em off somehow: tell them one of these little lies --

- ...tell them your accountant handles all of that and you'll have to call them first.

- ...tell them you never give out financial information on an incoming call and offer to call them back — a real company will give you a number; a scammer will push back.

- ...tell them your daughter/son handles your finances and you need to check with them first.

- ...tell them you're about to walk out the door and need to call them tomorrow.

Remember this: Real organizations don't pressure you to act during the call. If someone resists when you say you'll hang up and call the official number yourself — the one on your statement or the company's website — that resistance is your warning sign.

Final Thoughts

Fraud prevention for seniors is most effective when it happens early and calmly. Simple protections, clear communication plans, and steady financial habits can greatly reduce risk while preserving independence and dignity.

If you focus on preparation instead of fear, you (and your family) can approach financial safety with confidence, peace of mind, and the possibility that you're not going to be in that 75% of seniors who get scammed.

🔽 FAQs: Protecting yourself, red flags, resources for protection

Protecting seniors from financial fraud involves proactive steps: setting up bank account alerts, freezing credit,, shredding sensitive documents, and designating a trusted contact at financial institutions.

Key prevention strategies include never sharing personal information over the phone, ignoring high-pressure, unexpected requests, and educating seniors on common scams like grandparent or tech support scams.

Actions Before Money is Lost

- Secure Accounts & Information: Lock up checkbooks and bank statements. Shred all receipts and financial documents.

- Establish Trusted Oversight: Add a "trusted contact" to banking and investment accounts; this allows institutions to reach out if they suspect fraud. Consider setting up a durable power of attorney.

- Monitor Credit and Finances: Regularly review credit reports and bank statements for unauthorized activity. Freeze credit files to prevent new accounts from being opened.

- Build Financial Relationships: Get to know local bank staff, who are trained to spot signs of exploitation.

- Practice Active Prevention:

- Hang up on unsolicited calls and ignore high-pressure tactics.

- Register phone numbers on the National Do Not Call Registry.

- Never pay fees to receive "winnings" or sweepstakes prizes.

- Use credit cards instead of cash to maintain a paper trail.

Identifying Red Flags

- Unexplained withdrawals or missing belongings.

- Sudden changes in financial status or legal documents (wills, POA).

- A new "friend" or romantic partner suddenly taking an interest in finances.

- Pressure to send money immediately via wire transfer or gift cards. Office of the Comptroller of the Currency (OCC) (.gov) +4

Resources for Protection

- AARP Fraud Watch Network: Free resources to help seniors spot scams.

- Consumer Financial Protection Bureau (CFPB): Provides guides on protecting against financial exploitation.

- Federal Trade Commission (FTC): Use this to report scams and learn about current fraud tactics. Consolidated Community Credit Union +1

If you suspect fraud, report it immediately to local law enforcement, the bank, and the Adult Protective Services (APS).

Disclaimer: This article is for informational purposes only and is not legal or financial advice. Scam risks and complaint rates may change year to year. Always consult trusted professionals regarding financial or cybersecurity decisions.

{kind=link}