You’ve worked hard your whole life to create stability for yourself and your family. But without the right estate plan, a single illness, signature, or overlooked account could undo years of effort.

Smart Senior Daily asked attorney Lisa Cummings to share her expertise on this essential step in protecting your future. Here’s what she had to say about how to keep your money — and your wishes — exactly where they belong.

By Lisa A. Cummings, attorney and executive vice president at Cummings & Cummings.

Senior Estate Planning and Asset Protection Guide

For seniors, the top priority is planning for their incapacity in addition to disposition of assets after their death. Seniors should plan to execute a durable financial power of attorney, a health care proxy, a HIPAA release, and a living will so that trusted agents can act without court intervention.

A revocable living trust can centralize assets, provide continuity of management during illness, and reduce the risk of guardianship. They should also plan to transfer the legal title of key accounts to the trust and maintain an up-to-date pour-over will to capture any assets left outside the trust.

Beneficiary designations control retirement accounts and life insurance regardless of what a will says. Review every 401(k), IRA, annuity, and transfer on death designation, and elect per stirpes* where desired so that shares pass to grandchildren if a child predeceases you.

What is "per stirpes"?

Editor's note: “Per stirpes” means “by branch” — or, more simply, your family line gets your share if you pass away first.

Here’s how it works: If you leave something to your child per stirpes and that child dies before you do, their portion doesn’t disappear or get divided among the others. Instead, it goes to that child’s children — your grandchildren — in equal shares.

So if you have three children and one dies before you, that child’s share would automatically pass to their kids.

👉 Think of it like this: Your family tree still gets its branch, even if one limb is gone.

Be cautious with convenience joint accounts because the survivor will own 100 percent outright, which can unintentionally disinherit other heirs and expose funds to the co-owner’s creditors.

Asset protection relies on both legal structures and insurance

From an insurance viewpoint, be sure to purchase an umbrella liability policy, typically in the $1-$5 million range, and verify that all real estate rentals are held in limited liability companies with proper leases and reserves.

Understand your state’s homestead, retirement account, and life insurance creditor exemptions.

You can typically find those with a simple Google search such as “[Your state] homestead exemption statute” or “[Your state] creditor exemptions retirement accounts life insurance.”

Model long term care costs and evaluate financing through traditional long term care insurance, a hybrid life policy with a chronic illness rider, or a realistic earmark of portfolio assets.

Protecting yourself from being exploited

It's important to guard against elder financial exploitation by building process controls. The essential controls are:

Name a trusted individual to serve as contact on all brokerage accounts, enable alerts for large withdrawals or new payees, and require two people to approve wires over a set threshold.

Freeze credit at the bureaus, enable two-factor authentication, and store updated passwords and digital asset instructions in a secure vault that your fiduciaries can access.

Consider a professional co-trustee to provide oversight if family dynamics are strained or if assets are complex.

Coordinate estate planning with tax and retirement rules. Most non-spouse beneficiaries of IRAs must withdraw the account within 10 years, so trust language should be reviewed to avoid punitive tax results.

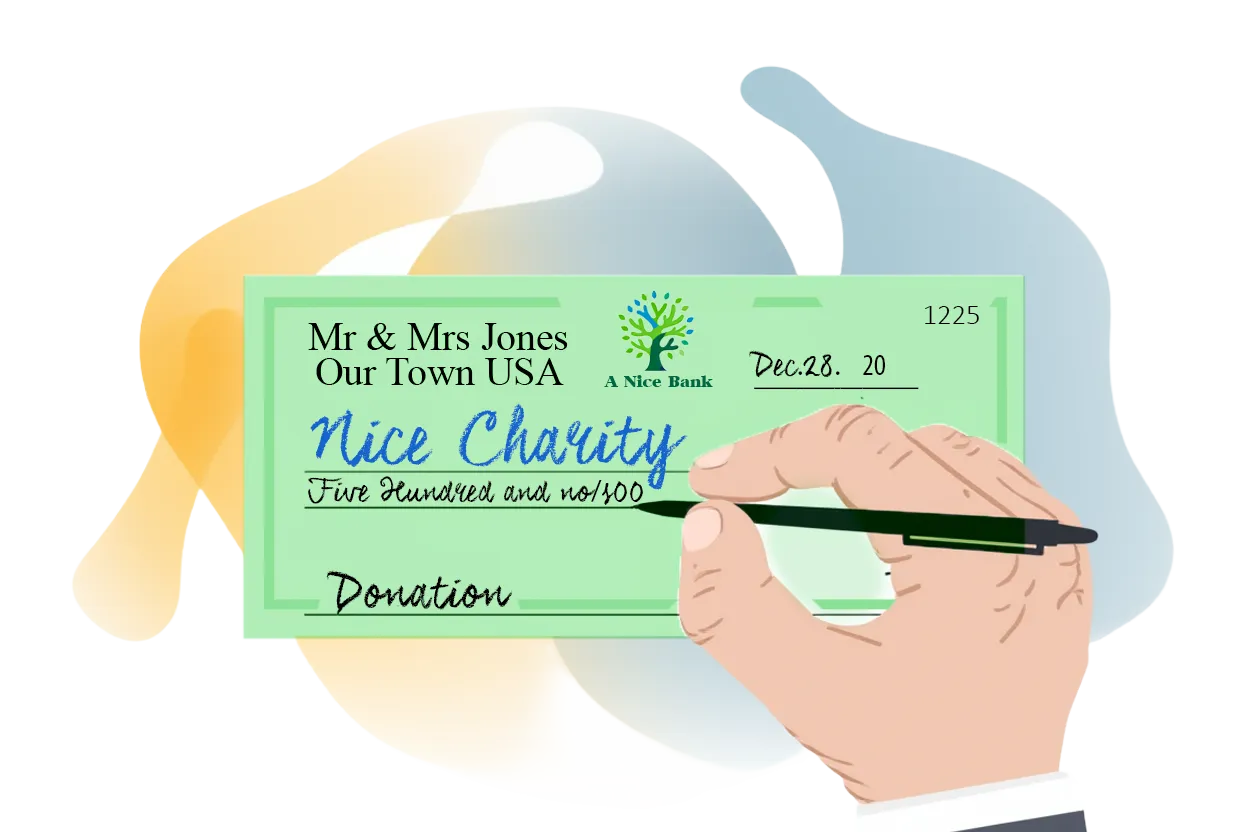

Where charitable giving is part of your plan, use qualified charitable distributions from IRAs once you reach the required minimum distribution age, which can reduce adjusted gross income while satisfying some or all the required minimum distribution.

For a child with special needs, use a third-party supplemental needs trust to preserve benefits. If you may need Medicaid later, avoid gifts that could trigger a penalty in the lookback period and obtain advice before transferring a residence.

A roadmap you can use

Recommended next steps for senior citizen asset and incapacity planning include the following:

- Compile a one page asset map with titling and beneficiary data

- Meet with an estate planning attorney to draft or update core documents and a revocable trust

- Schedule a portfolio review to align investments and insurance with spending and care plans

- Implement fraud safeguards and account alerts, and

- Calendar annual checkups to revisit family changes, tax laws, and long term care assumptions.

Lisa A. Cummings is an attorney and executive vice president at Cummings & Cummings. With more than four decades of legal experience, she has held senior and in-house counsel roles with major corporations including Halliburton, Dell Technologies, Walmart, Mercer, Kerr-McGee (now Occidental Petroleum), Cadbury Schweppes (now Keurig Dr Pepper), and others.

A graduate of the University of Oklahoma (B.S. in Accountancy; J.D., College of Law), she is a member of the Oklahoma Bar Association and the National Association of Elder Law Attorneys (NAELA). Her practice focuses on ERISA, executive compensation, employee benefits, and complex multi-state employment matters.

She divides her time between Bonita Springs, Florida, and Dallas, Texas, serving clients nationwide and internationally.

Disclaimer: This article is provided for informational purposes only and should not be considered legal, financial, or medical advice. Readers should consult qualified professionals regarding their individual circumstances. The views and opinions expressed are those of the contributor and do not necessarily reflect those of Smart Senior Daily. No payment, sponsorship, or other compensation was exchanged for this content.

{kind=link}