The Takeaway

- A new “senior bonus” deduction gives taxpayers 65+ extra room to reduce taxable income.

- Social Security benefits remain taxable, though fewer seniors may owe tax on them.

- Standard deductions and brackets rise across the board due to inflation indexing.

- Estate and long-term-care deductions are more generous for 2026.

- The law doesn’t change Medicare or Social Security benefit amounts.

A calmer tax season ahead — mostly

For 2026, the IRS has rolled out updated tax brackets and deductions under Revenue Procedure 2025-32, reflecting the One Big Beautiful Bill Act (OBBBA) passed in mid-2025.

While the name raised eyebrows, most of what’s in the new law simply extends or adjusts existing provisions rather than rewriting the tax code.

For seniors, the biggest headline is a new “senior bonus” deduction designed to give older taxpayers more breathing room — especially those living on fixed or modest incomes.

The new senior bonus deduction

Starting in 2026, taxpayers age 65 or older can take an additional deduction:

- $6,000 for single filers

- $12,000 for married couples if both spouses qualify

That’s on top of the regular standard deduction and the existing age-based add-on (currently $1,650 for singles and $1,650 per person for joint filers).

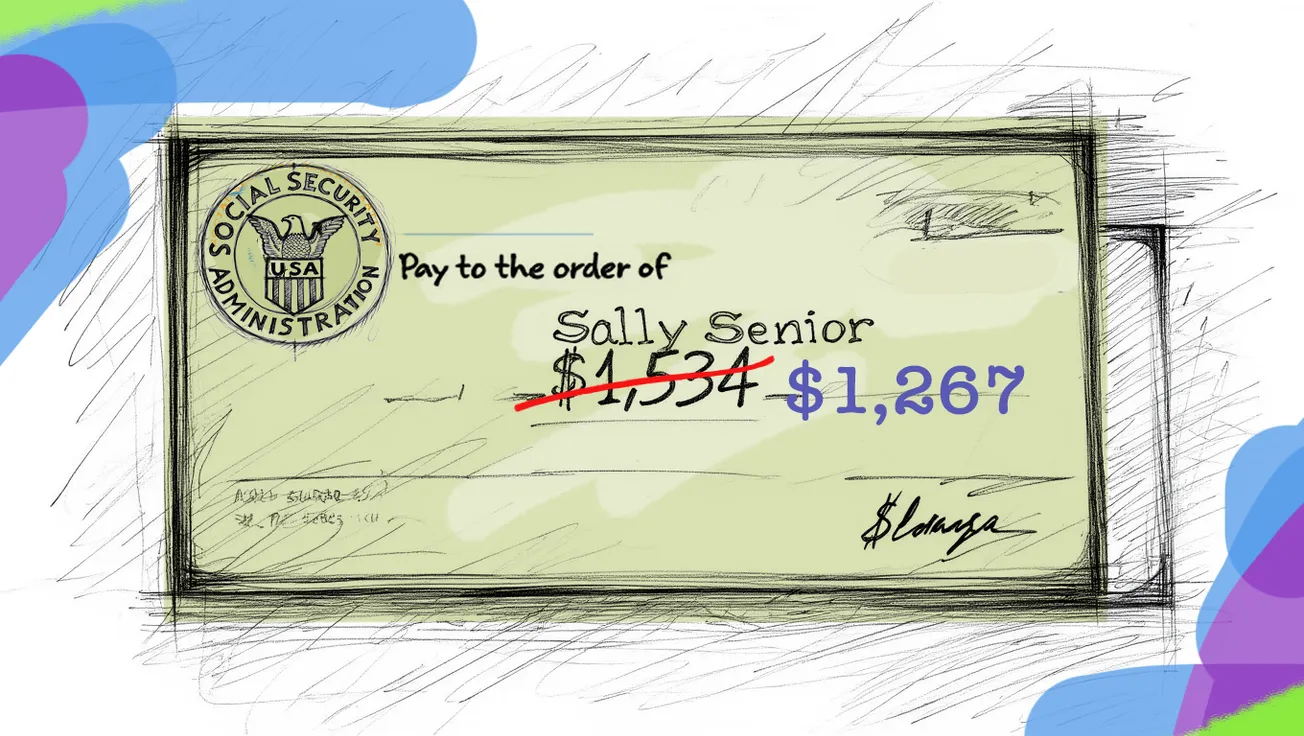

The extra write-off effectively lowers taxable income and can push many retirees below the level where Social Security benefits become taxable.

Example: A single retiree earning $32,000 — mostly from Social Security and small IRA withdrawals — would likely owe no federal income tax in 2026 after the combined deductions.

Side-by-side: 2025 vs. 2026

Other 2026 adjustments worth noting

- Long-term-care insurance premiums: The maximum deductible premium for people over 70 rises to $6,200.

- Estate and gift tax thresholds: The lifetime estate exemption increases to roughly $15 million per person (or $30 million for couples).

- Medical, education, and business deductions: All indexed upward modestly for inflation.

- Alternative Minimum Tax (AMT): Higher permanent exemption amounts mean fewer retirees will trigger it.

What hasn’t changed

Despite some social-media claims, the new law does not eliminate taxes on Social Security benefits.

The formula used to determine whether your benefits are taxable — based on combined income — remains the same.

However, with larger deductions, fewer seniors will cross those income lines.

Medicare premiums and benefit calculations are not tied to this law and continue to follow separate annual adjustments.

Bottom line

For most retirees, 2026 brings small but welcome relief. Lower-income seniors may owe nothing; middle-income couples will see lighter bills; higher-income retirees get a mild break but still pay taxes on Social Security and investment income.

The smartest move? Run a tax projection early in 2026 to see where you stand — and use those numbers to adjust withholdings or estimated payments before year-end.

Sources:

- IRS Revenue Procedure 2025-32 (irs.gov)

- Current Federal Tax Developments — Ed Zollars, CPA

- Kiplinger: How the Senior Bonus Deduction Works

Disclaimer: This article is for general informational purposes and not intended as tax or financial advice. Readers should consult a qualified tax professional regarding their personal circumstances.

{kind=link}