For many older Americans, Social Security is the closest thing we have to a steady paycheck in retirement. It shows up every month, right on time, and we build our budgets around it. Because of that, it’s easy to assume we already understand how it works.

But the truth is, social security benefits for seniors are often misunderstood. Small changes in income, work status, or family life can affect benefits in ways people don’t expect. And every year, a few rules quietly shift, leaving some seniors surprised when their check looks different than they planned.

This article isn’t about policy debates or fine print. It’s about the everyday issues that tend to catch seniors off guard—and what’s worth keeping an eye on.

What Many Seniors Get Wrong About Social Security

One common misunderstanding is the idea that Social Security is “set in stone” once you start collecting. While your basic benefit amount is based on your earnings history and the age you claim, several things can still affect what lands in your bank account each month.

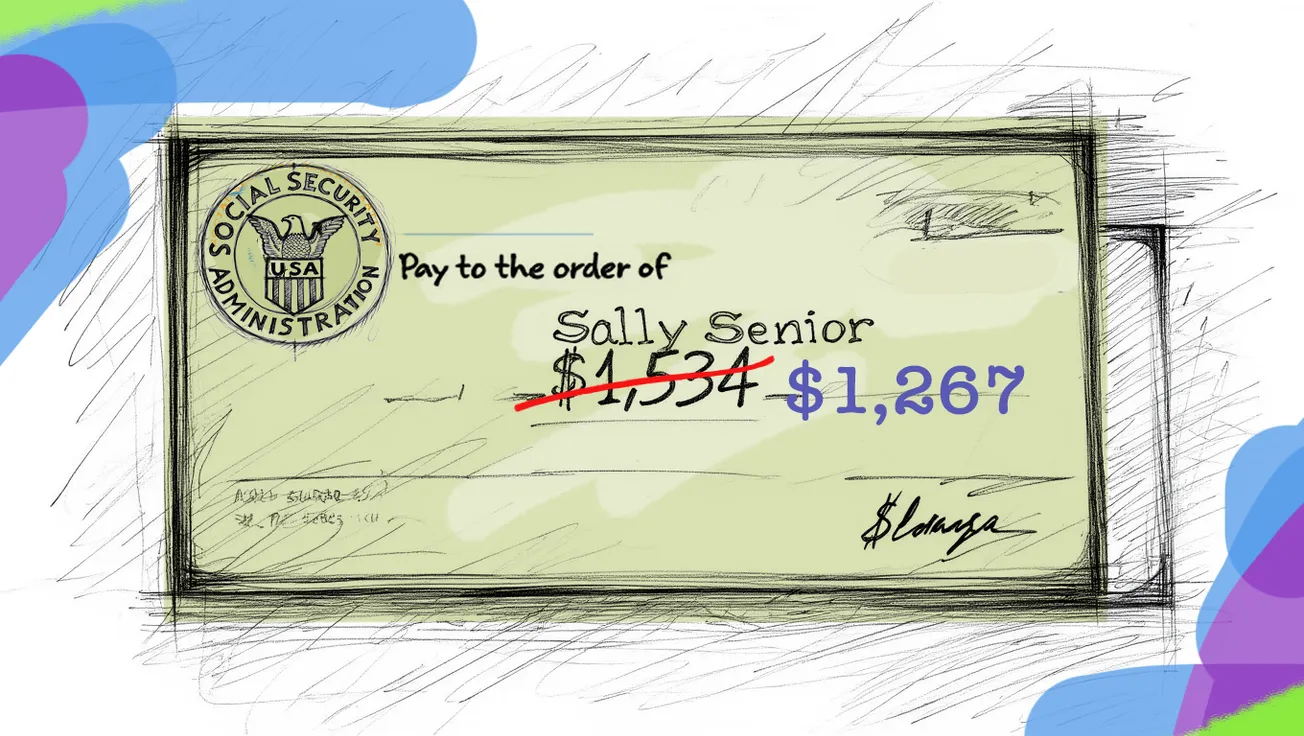

Another frequent assumption is that Social Security is tax-free. For some people, it is. For many others, it isn’t. Depending on your total income—from pensions, part-time work, withdrawals from retirement accounts, or even investment income—up to 85% of your Social Security benefits may be subject to federal income tax.

Many seniors are also surprised to learn that Medicare premiums are usually deducted directly from their Social Security check. If Medicare Part B or Part D premiums rise, your Social Security payment may shrink even if your benefit amount technically increased.

Cost-of-Living Adjustments: Helpful, But Not Perfect

Most seniors are familiar with the annual cost-of-living adjustment, often called a COLA. These increases are designed to help benefits keep up with inflation, and in recent years they’ve been more noticeable than usual.

Still, COLAs don’t always feel like much of a raise. Health care, housing, and insurance costs often rise faster than general inflation. So while your benefit might go up on paper, your day-to-day expenses can still outpace it.

It’s also important to remember that a higher benefit can trigger higher taxes or higher Medicare premiums, which may reduce the net increase you actually see.

Working While Collecting Benefits: A Common Source of Confusion

More seniors are working longer, whether by choice or necessity. Some take part-time jobs, consult, or return to work after retirement. This is where misunderstandings can get costly.

If you claim Social Security before reaching your full retirement age and continue working, there are limits on how much you can earn before benefits are temporarily reduced. This often surprises people who thought “retirement age” meant they could work freely.

Once you reach full retirement age, those earnings limits go away. You can earn as much as you like without reducing your monthly benefit. In some cases, continued work can even increase your benefit slightly over time if those earnings replace lower-earning years in your record.

The key point is that when you work matters just as much as how much you earn.

Life Events That Can Change Your Benefits

Social Security doesn’t operate in a vacuum. Major life changes can affect benefits, sometimes in ways people don’t anticipate.

Marriage is one example. Some seniors qualify for spousal benefits based on a current or former spouse’s work record. Others may lose eligibility depending on timing and circumstances.

Divorce can also come into play. If a marriage lasted at least ten years, a divorced spouse may still be eligible for benefits based on their ex-spouse’s earnings, even if that ex has remarried.

The death of a spouse is another major turning point. Survivor benefits follow different rules than retirement benefits, and many widows and widowers don’t realize they have options. In some cases, it makes sense to switch from one type of benefit to another.

These are emotional moments, and paperwork is often the last thing anyone wants to think about. Still, understanding how Social Security treats these events can prevent lost income.

Income That Can Quietly Reduce What You Take Home

Even if your benefit amount stays the same, your usable income might not.

Taxes, as mentioned earlier, are a big factor. But there are other deductions that may appear over time. Medicare premiums can rise, and higher-income seniors may pay additional amounts for coverage.

In rare cases, benefits can also be reduced to recover overpayments from past years. These situations can be stressful, especially if you weren’t aware of the issue beforehand.

Keeping records, opening mail from Social Security promptly, and asking questions early can help avoid surprises.

Why It Pays to Review Your Situation Periodically

Many seniors sign up for Social Security and never look back. That’s understandable. But a periodic review—especially after a life change—can make a real difference.

A change in work status, income, marital situation, or health coverage is often a good reason to check whether your current benefit choice still makes sense. What worked at 62 or 66 may not be the best option at 70.

You don’t need to become an expert. Sometimes simply asking, “Has anything changed that could affect my benefits?” is enough to uncover an issue worth addressing.

The Takeaway

- Social Security benefits for seniors can change based on income, work, taxes, Medicare costs, and life events

- Working before full retirement age can temporarily reduce benefits, while working after usually does not

- Marriage, divorce, or the loss of a spouse can open new benefit options many seniors don’t realize they have

- Reviewing your benefits after major life changes can help prevent unpleasant surprises

Social Security was never meant to be complicated, yet it often feels that way. A little awareness—and a willingness to ask questions—can go a long way toward making sure the benefits you’ve earned continue to support you the way you expect.

{kind=link}