If Social Security feels a little… off lately, well, you’re not hallucinating.

Despite SSA crowing that its customer service has gotten better, you plan a visit to where you've always gone to your local SSA office – but it's boarded-up and the phone number has gone dead, too.

The next minute, you’re hearing chatter that your Social Security benefits could take a haircut in a few years.

And then — out of nowhere — one of your retired government employee friends tells you that their monthly check went up for some unknown reason.

It’s a lot.

These question marks aren't part of a grand plan to do us all in, but rather, the happenstance of several smaller things hitting all at once. And depending on your situation, they could affect how you access your benefits, how much you receive, and even when you should file.

Let’s walk through the three biggest shifts — and what they mean for you.

1️⃣ "Where did my SSA office go?"

Last May, DOGE (the Elon Musk agency) put a target on the door of nearly 50 Social Security offices and readied them for closure, and in a hot minute, half of all seniors nationally were forced to drive at least 33 minutes to reach a field office. The total impact? Staffing cuts meant 2 million additional senior trips annually just to access existing benefits.

Now, SSA is getting greased up for another slide (or two or three) downward.

1️⃣ "Sorry, we're broke"

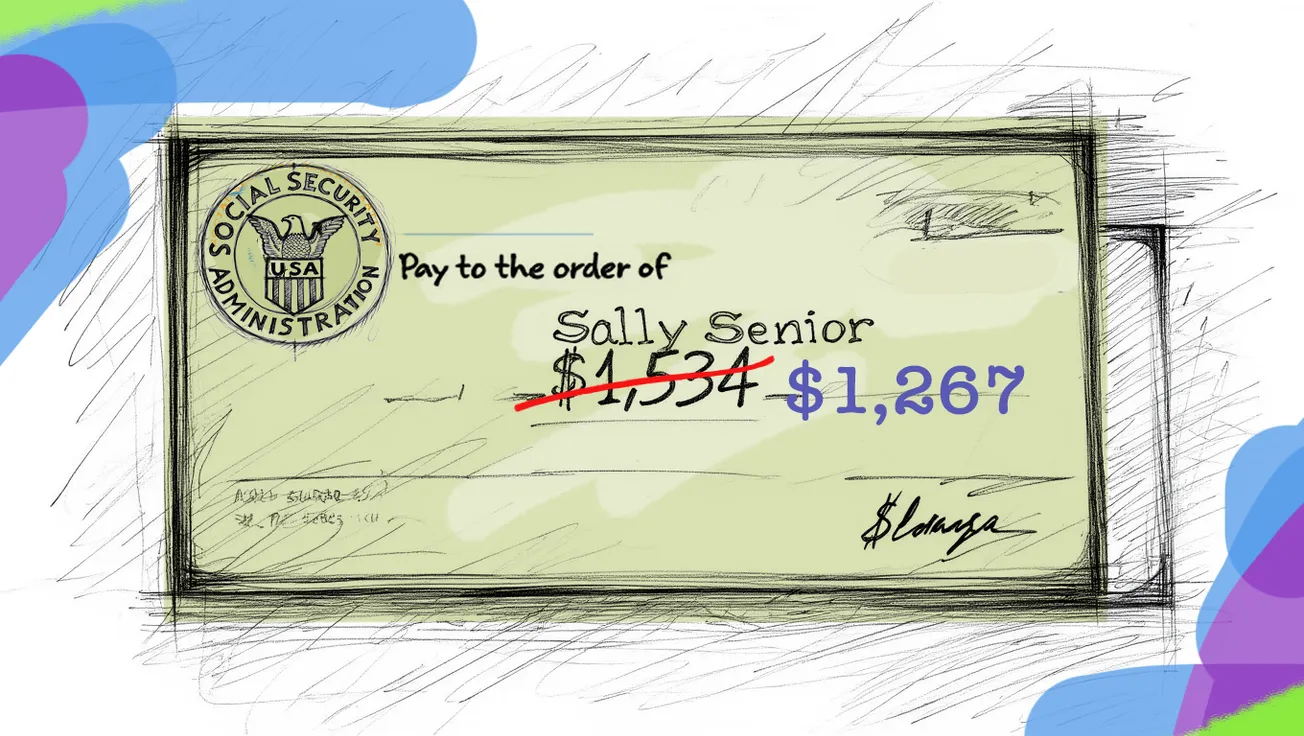

This time, the hand-wringing concerns what could happen to your Social Security benefits in six years if Congress doesn't act to replenish the trust fund that bolsters retirement benefits by 2032 when the fund could go broke.

If that date becomes reality, current projections estimate that anyone getting an SSA check could see that dollar amount shrink by 24% if Congress sits tight and does nothing.

The general feeling among experts is that if/when that happens, we're all going to take a cut in the size of our checks – particularly the poor among us, according to Mark Warshawsky, senior fellow at the American Enterprise Institute.

Should SSA applicants wait longer, then?

The psychological impact on those currently receiving benefits will be huge, but at least they're getting something. For the younger Seniors who are turning 62 and becoming eligible for benefits, there's even more number-crunching to do.

By waiting until full retirement age — 66 or 67 or holding on until they reach 70 – SSA beneficiaries may lock in bigger monthly payments.

2️⃣ "Why did the amount on my check go up?"

(... aka "The Social Security Rule Most Retirees Know Nothing About" section)

A little more than a year ago, Congress signed off on the Social Security Fairness Act, which killed the Windfall Elimination Provision and Government Pension Offset – a program which gave reduced benefits to public-sector workers.

In the stroke of that pen, anyone who was a public employee (and their spouses) lost the financial penalty that had been quietly docking their Social Security checks for years. Teachers. Firefighters. Police officers. Federal, state, and local government workers. If you spent any part of your career in a government job, Congress just handed you back the money that had been withheld — retroactively.

To its credit, SSA has already paid out $17 billion in retroactive lump sums to 3.1 million beneficiaries. Some recipients woke up to a surprise direct deposit with zero advance warning.

But here's the catch: millions more are still waiting. And a good number of them have no idea they're owed anything.

If you — or your spouse — ever held a government job and you haven't seen a bump in your check, here's what to to: log into your My Social Security account and compare your current benefit to what you were receiving before January 2025.

If the dollar amount on your check hasn't changed, you might think you're out of the woods, but don't assume everything is fine. Call SSA at 1-800-772-1213 because the money may already be yours — it's just that nobody's going to hand it to you without asking.

FAQs regarding recent Social Security Adminstration changes

Q: What exactly were the WEP and GPO — and why did they exist in the first place?

The Windfall Elimination Provision (WEP) reduced Social Security benefits for workers who also received a pension from a job not covered by Social Security — think teachers in certain states, or federal employees hired before 1984. The Government Pension Offset (GPO) hit spouses and survivors hard, reducing their Social Security spousal or survivor benefits by two-thirds of their government pension. Congress created both in the 1970s and '80s under the theory that these workers were "double dipping." Critics argued for decades that the penalties were unfair and often devastating — and Congress finally agreed.

Q: How do I know if I qualify for a retroactive payment?

If you worked in a federal, state, or local government job that came with a pension — and your Social Security benefit was reduced because of it — you likely qualify. Same goes for spouses and surviving spouses of public-sector workers whose own benefits were reduced. The simplest first step: log into your My Social Security account and check whether your monthly benefit has increased since January 2025. If it hasn't, that's your signal to call SSA.

Q: How much money could I actually be owed?

It varies widely. Some retirees have already received lump-sum retroactive payments of several thousand dollars. The average retroactive payment across the 3.1 million beneficiaries paid so far works out to roughly $5,500 — but individual amounts depend on how long you were subject to the WEP or GPO and how much was withheld. Your ongoing monthly benefit should also be higher going forward.

Q: What if I'm the surviving spouse of a public employee — does this apply to me?

Yes — and this group in particular has been underpaid the longest. Surviving spouses who were subject to the GPO had their survivor benefits cut by two-thirds of their late spouse's government pension, sometimes wiping out their benefit entirely. That reduction should now be eliminated. If you haven't seen a change in your benefit, contact SSA immediately.

Q: I haven't received anything yet. What should I do right now?

Don't wait. Call SSA at 1-800-772-1213 (TTY: 1-800-325-0778), or visit your local field office if one is still open near you. Have your Social Security number handy, and be ready to explain that you believe you were subject to the WEP or GPO. If you hit a wall and don't get the answers you need, the Medicare Rights Center and your state's SHIP (State Health Insurance Assistance Program) counselors can also help you navigate the process at no cost.

Disclaimer: The information in this article is for educational purposes only and reflects conditions as of the date of publication. Social Security rules, benefit amounts, and program structures are subject to change. Smart Senior Daily is not a financial or legal advisor. For guidance specific to your situation, contact the Social Security Administration directly at 1-800-772-1213 or visit ssa.gov, or consult a qualified financial planner or elder law attorney.

{kind=link}